Sector Analysis

Posted On: February 27, 2026

Indian Construction Sector Analysis | Feb 2026

Industry Overview

The construction sector is a key driver of India’s infrastructure growth, contributing ~8% of GDP in FY25 (Economic Survey 2025–26). It covers housing, roads, railways, ports, airports, and industrial infrastructure. As of Dec 2025, MoSPI reported 11 core infrastructure sectors grew by 6.8%, with construction being a major contributor. The sector is central to the government’s National Infrastructure Pipeline (NIP) and PM Gati Shakti Master Plan.

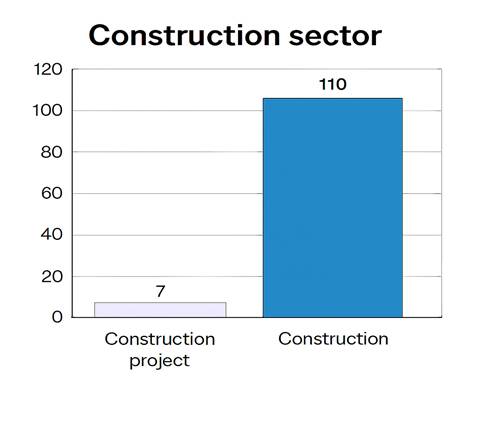

The construction sector is composed of two key industries. The Construction industry accounts for 110 companies, making it the dominant segment, while the Construction projects industry includes 7 companies, representing a much smaller share.

Market Size and Growth Metrics

- Contribution to GDP (FY25): ~8% (MoSPI/Economic Survey).

- Employment Share: ~12% of workforce engaged in construction (PLFS, Jan 2026).

- Infrastructure Projects (Dec 2025): 1,500+ projects above ₹150 crore under monitoring (MoSPI).

- Forecast: Construction sector expected to grow at 7–8% annually until 2030, driven by housing, transport, and industrial corridors.

Market Dynamics and Drivers

- Growth Drivers: Urbanization, housing demand, infrastructure investment, industrial corridors.

- Supply Chain: Cement, steel, construction equipment, skilled/unskilled labor.

- Technological Trends: Smart cities, prefabricated construction, green buildings, digital project management.

- Consumer Trends: Rising demand for affordable housing, commercial real estate, and sustainable infrastructure.

Competitive Landscape

- Major Players: L&T, NBCC,

- Public Sector: NHAI, CPWD, Indian Railways, Smart City Mission.

- Supplier Power: Moderate; cement and steel prices affect project costs.

- Buyer Power: High, with government as the largest client.

- Threat of Substitutes: Limited, though prefabricated and modular construction methods are emerging.

Regulatory Measures

- National Infrastructure Pipeline (NIP): ₹111 lakh crore investment plan till 2030.

- PM Gati Shakti Master Plan (2025): Integrated infrastructure planning across transport, logistics, and energy.

- Affordable Housing Policy (2025): Incentives under PMAY-Urban and PMAY-Gramin.

- MoSPI Infrastructure Reports (Dec 2025): Monitoring of large projects above ₹150 crore.

Macro Environmental Analysis

- Construction sector growth tied to government capital expenditure.

- Budget 2026 increased allocation for roads, railways, and housing.

- Rising cement and steel prices pose cost challenges.

- Climate change risks driving demand for sustainable and green buildings.

- Urbanization and smart city projects fueling demand.

SWOT Analysis

Strengths

- Large workforce and strong domestic demand.

- Government-backed infrastructure pipeline.

- Expanding housing and transport projects.

Weaknesses

- Cost escalation due to raw material prices.

- Project delays and regulatory hurdles.

- Dependence on government spending.

Opportunities

- Smart cities and green buildings.

- Prefabricated and modular construction.

- Public-private partnerships (PPP).

- Industrial corridors and logistics hubs.

Threats

- Global commodity price volatility.

- Climate risks affecting project timelines.

- Financial stress in real estate developers.

- Regulatory delays in land acquisition.

Future Outlook

- Construction sector projected to reach USD 1 trillion by 2030.

- Housing demand expected to grow at 6–7% annually.

- Infrastructure projects under NIP and Gati Shakti to drive growth.

- Focus on green buildings, smart cities, and digital project management.

Conclusion

India’s construction sector is a pillar of infrastructure-led growth, contributing significantly to GDP and employment. With strong government investment under NIP and Gati Shakti, the sector is poised for sustained expansion. Challenges such as raw material costs, project delays, and regulatory hurdles must be addressed to ensure resilience and competitiveness under the Viksit Bharat 2047 vision.

Sources

- Ministry of Statistics & Programme Implementation (MoSPI Infrastructure Reports, Dec 2025–Feb 2026),

- Economic Survey 2025–26,

- Open Government Data (OGD) Platform India,

- National Data & Analytics Platform (NDAP).

What is xCalData?

xCalData is a Made in India AI powered investment research platform called RHOMB.

Using multilayered neural network, RHOMB analyses over 150+ technical ratios, 150+ candlestick chart patterns and over 40 fundamental ratios of each stock.

RHOMB forecasts the stock price movement for the next few days and determines buy, sell, hold or wait.

How accurate is xCalData?

xCalData publishes the accuracy of the past trades for each stock to enable an informed decision.

Is xCaldata an Algo trading platform?

No, xCalData is not an algotrading platform. User decides when to buy or sell including, we only provide inputs for the decision.

Download the app for further stock level insights: https://open.xcaldata.com/apps/

Checkout the trades and detailed insights in the app

Popular Posts

-

Stock of Interest . August 23, 2024

#HSCL (NSE) Stock Report | 23 Aug 2024

-

Stock of Interest . August 23, 2024

Add Zerodha trading account to xCalData

-

Stock of Interest . August 23, 2024

What is xCalData , how to use it and how accurate is it?

-

Stock of Interest . August 23, 2024

Jurik Moving Average (JMA): A Profit Trading Insight