Sector Analysis

Posted On: February 27, 2026

Indian Energy Sector Analysis | Feb 2026

Industry Overview

India is the third-largest energy consumer globally, with total installed power capacity of ~510 GW (Jan 2026, NPP). Renewable energy contributes ~263 GW, accounting for over 51% of installed capacity (MNRE). The government’s long-term vision under IESS 2047 is to achieve net-zero emissions by 2070, with renewables, green hydrogen, and energy efficiency as key drivers.

Market Size and Growth Metrics

- Installed Capacity (Jan 2026): ~510 GW

- Thermal (Coal, Gas, Lignite): ~247 GW

- Hydro (Large + Small): ~56 GW

- Nuclear: ~8.7 GW

- Renewables (Solar, Wind, Biomass, Small Hydro, Waste-to-Energy): ~263 GW

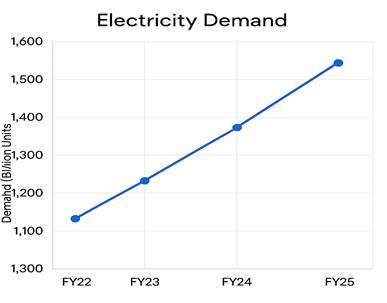

- Electricity Demand (FY25): ~1,600 BU (CEA/NPP).

- Renewable Generation (FY25–26): ~403 BU, nearly double compared to 2014 (MNRE).

- Forecast: Energy demand expected to grow at 4–5% annually until 2030.

Market Dynamics and Drivers

- Growth Drivers: Rising industrial demand, renewable expansion, EV adoption, rural electrification.

- Supply Chain: Strong coal base, expanding solar/wind manufacturing, LNG imports for gas-based power.

- Technological Trends: Smart grids, battery storage, green hydrogen, carbon capture.

- Consumer Trends: Rooftop solar adoption, EV charging demand, digital energy management.

Competitive Landscape

- Major Players: NTPC, Power Grid Corporation, Adani Green, Tata Power, NHPC.

- New Entrants: Green hydrogen startups, battery storage firms.

- Supplier Power: Moderate; coal and LNG imports remain critical.

- Buyer Power: High, with DISCOMs and industrial consumers demanding affordable tariffs.

- Threat of Substitutes: Growing due to renewables, distributed generation, and energy efficiency solutions.

Regulatory Measures

- Electricity Act Amendments (2025): Strengthened Renewable Purchase Obligations (RPOs).

- National Green Hydrogen Mission (2025): ₹19,744 crore outlay for hydrogen production and infrastructure.

- Economic Survey 2025–26: Emphasis on energy transition, fiscal support for renewables and DISCOM reforms.

- NITI Aayog IESS 2047: Pathways for achieving 450 GW renewable capacity by 2030.

Macro Environmental Analysis

- Coal remains dominant (~70% of electricity generation).

- Renewable energy growth strong, but grid integration challenges persist.

- Budget 2026 allocated higher investments for transmission infrastructure and storage.

- Global energy price volatility impacts LNG and coal imports.

- India’s climate commitments driving policy focus on clean energy.

SWOT Analysis

Strengths

- Large installed capacity with strong renewable growth.

- Government-backed energy transition policies.

- Expanding transmission and distribution infrastructure.

Weaknesses

- High dependence on coal imports.

- DISCOM financial stress.

- Grid integration challenges for renewables.

Opportunities

- Green hydrogen and battery storage.

- Rooftop solar and distributed generation.

- EV charging infrastructure expansion.

- International energy partnerships.

Threats

- Global fuel price volatility.

- Climate risks impacting coal supply chains.

- Regulatory delays in renewable integration.

- Competition from global renewable leaders

Future Outlook

- Installed capacity projected to cross 600 GW by 2030, with renewables >50%.

- Energy demand expected to grow at 4–5% annually.

- India aims for net-zero emissions by 2070, with energy sector as the key driver.

- Focus on green hydrogen, storage, and smart grids to ensure sustainable growth.

Conclusion

India’s energy sector is at the heart of its economic and climate strategy. While coal remains dominant, rapid renewable expansion, green hydrogen initiatives, and government-backed reforms are reshaping the sector. Challenges such as import dependence, DISCOM stress, and grid integration must be addressed to ensure a resilient, sustainable energy future under the Viksit Bharat 2047 vision.

Source

- National Power Portal (Installed Capacity & Generation Data, Jan 2026)

- Ministry of New & Renewable Energy (MNRE Physical Achievements, Jan 2026)

- Economic Survey 2025–26 (India Budget)

- NITI Aayog – India Energy Security Scenarios (IESS) 2047 v3.0

What is xCalData?

xCalData is a Made in India AI powered investment research platform called RHOMB.

Using multilayered neural network, RHOMB analyses over 150+ technical ratios, 150+ candlestick chart patterns and over 40 fundamental ratios of each stock.

RHOMB forecasts the stock price movement for the next few days and determines buy, sell, hold or wait.

How accurate is xCalData?

xCalData publishes the accuracy of the past trades for each stock to enable an informed decision.

Is xCaldata an Algo trading platform?

No, xCalData is not an algotrading platform. User decides when to buy or sell including, we only provide inputs for the decision.

Download the app for further stock level insights: https://open.xcaldata.com/apps/

Checkout the trades and detailed insights in the app

Popular Posts

-

Stock of Interest . August 23, 2024

#HSCL (NSE) Stock Report | 23 Aug 2024

-

Stock of Interest . August 23, 2024

Add Zerodha trading account to xCalData

-

Stock of Interest . August 23, 2024

What is xCalData , how to use it and how accurate is it?

-

Stock of Interest . August 23, 2024

Jurik Moving Average (JMA): A Profit Trading Insight