Sector Analysis

Posted On: February 27, 2026

Oil Gas & Consumable Fuels Sector Analysis | Feb 2026

Industry Overview

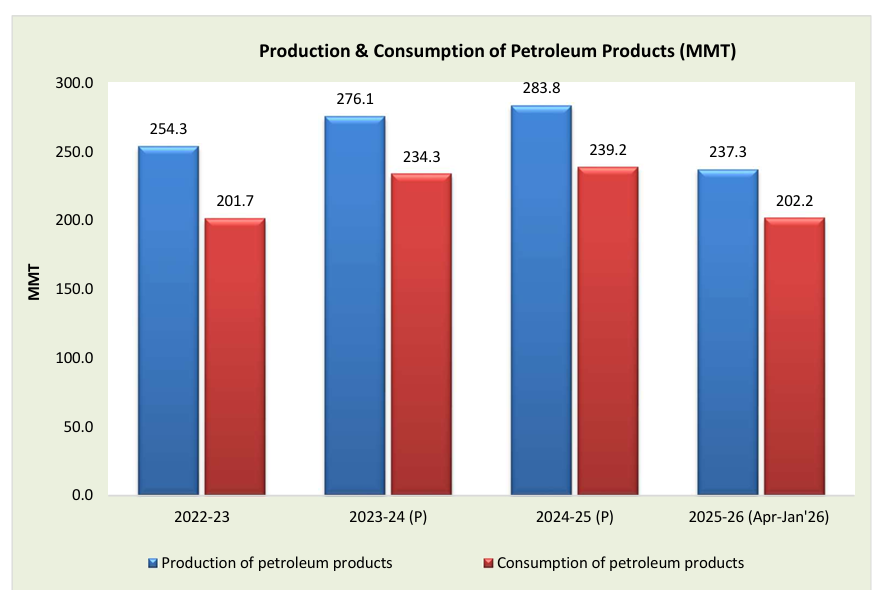

India is the world’s third-largest oil consumer and fourth-largest refiner, with refining capacity of 258.1MMTPA (FY24). The oil & gas sector contributes significantly to India’s energy security, accounting for ~35% of primary energy consumption. The government aims to increase domestic crude production to 100 MMT and natural gas output to 100 BCM by 2047, while expanding refining capacity to 450 MMTPA under the Viksit Bharat 2047 vision.

Market Size and Growth Metrics

- Crude Oil Production (FY25): 28.7 MMT (PPAC data).

- Natural Gas Production (FY25): ~36 BCM.

- Refining Capacity (FY24): 258.1 MMTPA across 23 refineries (19 PSU, 3 private, 1 JV).

- Crude oil import (2025): 243.2 MMT

- Forecast: Oil demand projected to grow at 3–4% annually; gas demand expected to double by 2030.

source : PPAC

Market Dynamics and Drivers

- Growth Drivers: Rising energy demand, infrastructure expansion, cleaner fuels, LNG imports.

- Supply Chain: Strong refining base, pipeline network, LNG terminals.

- Technological Trends: Green hydrogen, biofuels, CCUS (Carbon Capture, Utilization & Storage).

- Consumer Trends: Rising demand for LPG, CNG, and cleaner fuels.

Competitive Landscape

- Major Players: ONGC, OIL, IOCL, BPCL, HPCL, Reliance Industries.

- New Entrants: Private LNG importers, renewable-integrated energy firms.

- Supplier Power: Moderate; dependence on crude imports (~85% of demand).

- Buyer Power: High, with consumers sensitive to fuel prices.

- Threat of Substitutes: Growing due to EV adoption, renewable energy, and biofuels.

Regulatory Measures

- Hydrocarbon Exploration Licensing Policy (HELP): Open acreage licensing for exploration.

- Gas Pricing Reforms (2025–26): PPAC notified revised domestic gas prices.

- Biofuel Policy (2025): Target of 20% ethanol blending by 2025.

- Economic Survey 2025–26: Emphasis on energy security, fiscal support for oil marketing companies.

Macro Environmental Analysis

- India imports ~85% of crude oil, making it vulnerable to global price volatility.

- LNG imports rising, with terminals expanding capacity to meet demand.

- NITI Aayog’s IESS 2047 highlights pathways for net-zero by 2070, with oil & gas sector transitioning to cleaner fuels.

- Budget 2026 allocated higher investments for strategic petroleum reserves and pipeline infrastructure.

SWOT Analysis

Strengths

- Large refining capacity and strong PSU presence.

- Expanding pipeline and LNG infrastructure.

- Strategic petroleum reserves enhancing energy security.

Weaknesses

- Heavy dependence on crude imports (~85%).

- Low domestic production growth.

- Price volatility impacting fiscal balance.

Opportunities

- Expansion of LNG, biofuels, and green hydrogen.

- Refining capacity expansion to 450 MMTPA by 2047.

- Integration with renewable energy and CCUS technologies.

Threats

- Global oil price shocks.

- Geopolitical risks in supply chains.

- Rising competition from renewables and EVs.

Future Outlook

- Gas demand projected to double by 2030, driven by power, fertilizer, and city gas distribution.

- India aims for energy independence by 2047, with oil & gas sector playing a transitional role.

- Focus on diversification: biofuels, hydrogen, LNG, and CCUS.

Conclusion

India’s oil and gas sector is resilient but import‑heavy, with oil demand peaking in the medium term and gas emerging as the growth driver. The future competitiveness of the sector will depend on domestic production enhancement, infrastructure expansion, and integration with clean energy pathways.

Sources

- Ministry of Petroleum & Natural Gas – Annual Report 2025–26

- Petroleum Planning & Analysis Cell (PPAC) – Ready Reckoner FY25–26

Supplies verified statistics on petroleum product consumption, pricing reforms, and import dependency. - Economic Survey 2025–26 (Government of India, Ministry of Finance)

- NITI Aayog – India Energy Security Scenarios (IESS) 2047

- Hydrocarbon Exploration Licensing Policy (HELP)

- National Biofuel Policy (2025)

- Budget 2026 (Union Budget, Ministry of Finance) – Allocations for strategic petroleum reserves and pipeline infrastructure.

What is xCalData?

xCalData is a Made in India AI powered investment research platform called RHOMB.

Using multilayered neural network, RHOMB analyses over 150+ technical ratios, 150+ candlestick chart patterns and over 40 fundamental ratios of each stock.

RHOMB forecasts the stock price movement for the next few days and determines buy, sell, hold or wait.

How accurate is xCalData?

xCalData publishes the accuracy of the past trades for each stock to enable an informed decision.

Is xCaldata an Algo trading platform?

No, xCalData is not an algotrading platform. User decides when to buy or sell including, we only provide inputs for the decision.

Download the app for further stock level insights: https://open.xcaldata.com/apps/

Checkout the trades and detailed insights in the app

Popular Posts

-

Stock of Interest . August 23, 2024

#HSCL (NSE) Stock Report | 23 Aug 2024

-

Stock of Interest . August 23, 2024

Add Zerodha trading account to xCalData

-

Stock of Interest . August 23, 2024

What is xCalData , how to use it and how accurate is it?

-

Stock of Interest . August 23, 2024

Jurik Moving Average (JMA): A Profit Trading Insight